Dear Fed,

Macro Man speaks to a lot of well-informed, knowledgeable punters. Many of you (collectively on the FOMC) know some of these very people. They are smart, and they spend a lot of time analyzing you and trying to understand your way of thinking.

And last night, after you changed this:

The Committee will maintain the target range for the federal funds rate at 0 to 1/4 percent and continues to anticipate that economic conditions are likely to warrant exceptionally low levels of the federal funds rate for an extended period

to this:

The Committee will maintain the target range for the federal funds rate at 0 to 1/4 percent and continues to anticipate that economic conditions, including low rates of resource utilization, subdued inflation trends, and stable inflation expectations, are likely to warrant exceptionally low levels of the federal funds rate for an extended period

the interpretation of this group of well-informed observers ranged from “as dovish as it could be” to “man, that’s pretty hawkish.”

Please. I know Greenspan once said that if his meaning was clear, you hadn’t understood him properly. But where did that get us? Seriously, one shouldn’t need to employ a literary theorist to figure out what you’re saying. Ditch the stupid word games and speak clearly. Compared to A students like the RBNZ:

In contrast to current market pricing, we see no urgency to begin withdrawing monetary policy stimulus, and we expect to keep the OCR at the current level until the second half of 2010

and the Bank of Canada:

Conditional on the outlook for inflation, the target overnight rate can be expected to remain at its current level until the end of the second quarter of 2010 in order to achieve the inflation target

you collectively get a big fat F for your essay.

Sincerely, Macro Man

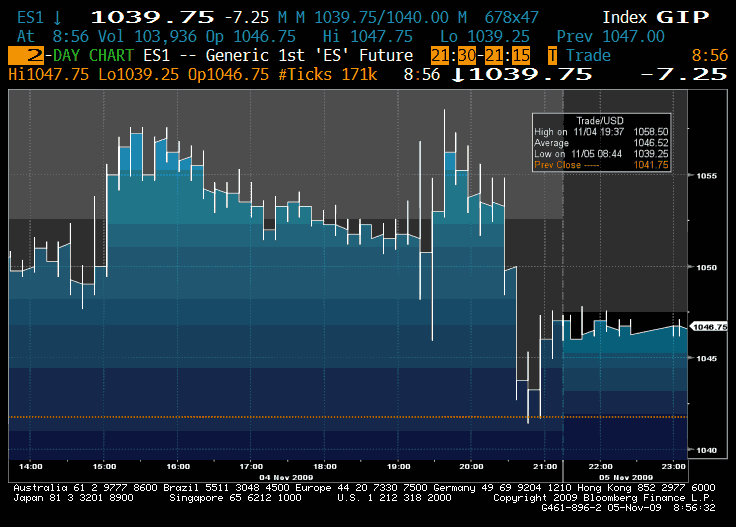

Given the opacity of the Fed’s communication strategy (in terms of using blunt phrases to convey very nuanced shifts), is it any wonder that the market’s reaction was as schizophrenic as it was?

(click to enlarge)

And given that schizophrenia, is it any wonder that a “signal” trader like Macro Man is struggling amongst all the noise? Taking an introspective step backwards last night, Macro Man concluded that one of his primary problems is that he is reacting to short term price swings, rather than anticipating. The problem with reacting is two-fold: conviction is necessarily lower than it would be with a well-thought out macro view, and the lack of serial correlation leads to a lot of top-and-tailing. Macro Man has had enough.

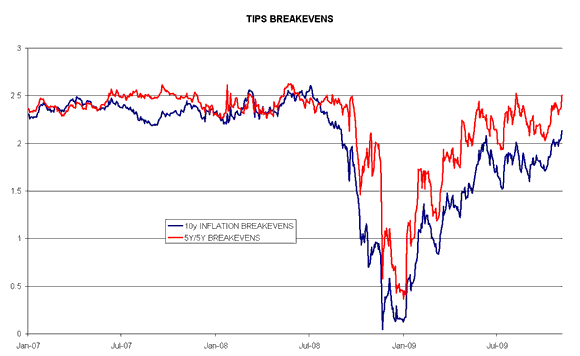

Anyhow, the primary feature of the Fed’s semiotic parlour game was the introduction to conditionality to the “extended period” clause. The first two conditions- the output gap and actual inflation- would not appear to merit tightening for the foreseeable future. The third- inflation expectations- could prove to be a bit more problematic, though 10 year breakevens are still below their pre-crisis levels. Still, the recent normalization is striking!

QE or not QE? That is the question. Whether ’tis nobler in the mind to suffer the slings and arrows of outrageous banking, or to take arms against a sea of troubles, and buy Gilts to end them?

-Hamlet’s Soliloquy, by the Bard of Avon Swerve of Lomard Street

The highlight of the day today will be the Bank of England’s policy announcement at noon local time. An extension of QE has been widely bandied about in the press, particularly in the wake of the recent GDP shocker. Ex-MPC’er David Blanchflower certainly favors more; at this juncture there appears to be little firm consensus, however, with some shops calling for nowt and others calling for £50 bio more gilt buying, plus a cut in the reserve deposit rate. If the latter were enacted, one would presume that sterling would get trashed.

Whether the Bank should do more QE is, of course, another question: the GDP figures scream “yes!”, but more forward looking indicators suggest a more positive trajectory for the economy.

Either way, there should be some fireworks. And let’s not forget Jean-Claude, ostensibly relegated to the role of bit-part actor in this week’s drama, but always capable of stealing the show at his press conference. Needless to say, Macro Man isn’t getting his hopes up for a spot of plain speaking there…..

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply