The Wall Street Journal repeats the unhappy news:

“Companies across the economy are holding off on hiring even as the profit outlook improves, amid economic uncertainty and their own success at raising productivity in rough waters.

“Hiring always lags behind in economic recoveries, but the outlook this time is worse, many economists say. Most forecasters now expect a prolonged period of high unemployment, even though the government is expected to report next week that the economy grew in the third quarter, after four quarters of contraction.”

I’d like to be able to contradict what most forecasters expect, but we at the Atlanta Fed have been building the case for a similar outcome on macroblog. Here are few salient points from previous posts:

Job opportunities are scarce. (Oct. 14, 2009)

“At the end of August there were estimated to be fewer than 2.4 million job openings, equal to only 1.8 percent of the total filled and unfilled positions—a new record low.”

This development could, of course, turn around as business activity picks up, but there is more than a little evidence that some structural impediments are afoot.

Job losses have been disproportionately concentrated in small businesses. (Oct. 6, 2009)

As Melinda Pitts pointed out a few weeks back, businesses with fewer than 50 employees account for about one third of net employment gains in expansions. They have accounted for about 45 percent of job losses since the beginning of this recession. Given that these are the types of businesses most likely to be dependent on bank lending—and given that bank lending does not appear poised for a rapid return to being robust—the prognosis for an employment recovery in these businesses is a question mark.

The share of workers reporting that they have been involuntarily cut back to part-time is at a recorded high. (Aug. 14, 2009)

“… the increase in people reporting that they are involuntarily working part-time rather than full-time is considerably higher in this recession than in past recessions. Although the increase in these workers has moderated some since the spring of this year, the number of people in the category of working part-time for economic reasons remains at 8.8 million, well above the level of past contractions in both absolute and relative terms.”

One potential implication of this fact is that firms probably have the capacity to expand production without hiring new workers (or increasing worker productivity). All these firms have to do is give more hours to existing workers, who have indicated they would be plenty eager to have them. Good for them—and good for GDP growth—but not much help on the employment front.

Here is one additional concern that we have not previously emphasized:

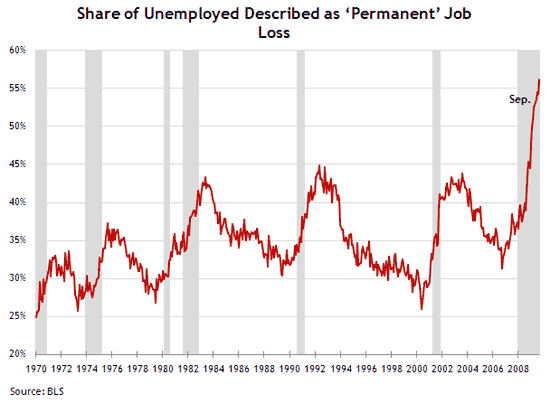

The percentage of employee separations labeled permanent is at a recorded high.

Underneath the usual total unemployment numbers are the reasons an individual is unemployed: You are on temporary layoff; you quit your job; you have reentered the labor market and have yet to find a job; or you are entering the job market for the first time and have yet to find a job. Or, finally, you have been permanently separated from your previous employer, who has no expectation of hiring you back.

The last category is the dominant reason for unemployment at this time. That might not seem surprising, but it actually is. Never, in the six recessions preceding the latest one, did permanent separations account for more than 45 percent of the unemployed. The current percentage stands at 56 percent as of September and appears to be still climbing:

Of course, none of this is proof positive that we are in for a “jobless recovery,” but, to me, the odds appear to be increasing.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply