McLean, VA – Freddie Mac today released the results of its Primary Mortgage Market Survey in which the 30-year fixed-rate mortgage (FRM) averaged 4.92% with an average 0.7 point for the week ending October 15, 2009, up from last week when it averaged 4.87%. Last year at this time, the 30-year FRM averaged 6.46%.

“Mortgage rates rose slightly over the week, but rates on 30-year fixed mortgages remained below 5% for the third consecutive week,” said Frank Nothaft, Freddie Mac vice president and chief economist. “Homeowners are taking advantage of these low rates to refinance their current balances. Over the past five weeks ending October 9, more than three out of five mortgage applications were for refinancing, according the Mortgage Bankers Association.

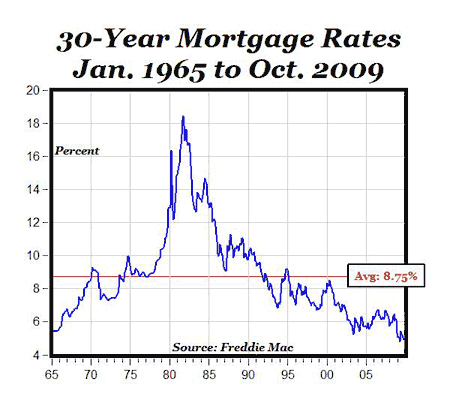

MP: The chart above shows monthly mortgage rates back to 1965 to help put the current situation into perspective. There has never been any comparable period since the 1960s when 30-year mortgage rates have remained so low for so long. On a weekly basis, mortgage rates have been below 5% for fourteen weeks so far in 2009, including the last three weeks.

Mortgage rates climbed to historically high levels in the late 1970s and early 1980s because of historically high levels of actual inflation and expected inflation.

If inflationary pressures are now building up in the U.S. economy, and expected inflation is expected to be higher, why isn’t are those inflationary pressures being reflected in the bond market (see related CD post) or the mortgage market? For those worried about future inflation, this would be a great time to re-finance your mortgage at the current rates of below 5% for 30 years. All it would take is an actual inflation rate of above 5% sometime during the next 30 years to result in a negative, real interest rate, the best of all possible worlds for a borrower (it’s like borrowing $100 from a bank, but only have to pay back $99, $95 or $90 in real dollars).

******

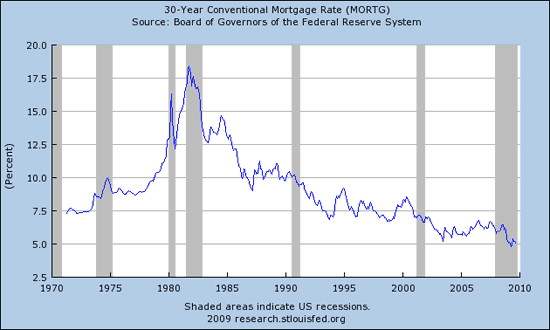

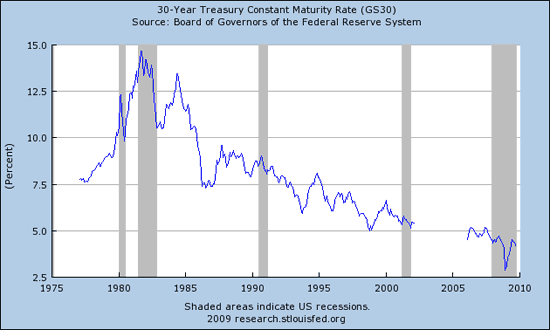

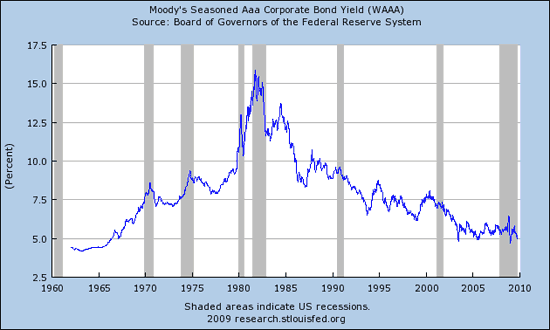

Update: Above I suggested that historically low 30-year mortgage rates reflected relatively low market expectations of future inflation. Some commenters (and Robert Shiller this afternoon on CNBC) pointed out that the Fed is buying mortgage securities, which is temporarily keeping 30-mortgage rates low, rather than low inflation expectations keeping rates low.

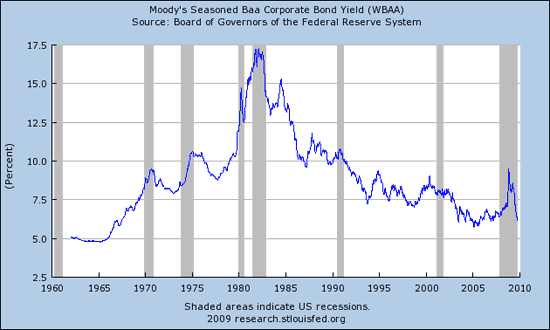

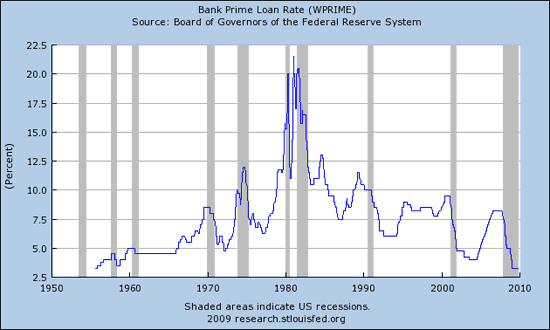

But the charts below show that other long-term rates (30-year Treasury bond, 30-year AAA corporates and 30-year Baa corporates) are historically low, as well as the prime rate being historically low, and these low rates wouldn’t necessarily have anything to do with Fed purchases.

Question: How could all of these long-term rates be so low if there were inflationary pressures building up in the economy, which would lead to higher expected future inflation, and higher nominal long-term interest rates, and not historically low long-term rates?

Charts: St. Louis Fed

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply