Gavyn Davies reviews the evidence on the apparent slowing of US economic activity and concludes:

So is the US slowdown for real? Yes, but it is not yet very severe — and some of it is the result of the temporary inventory correction, and some to the rising dollar. Unless it grows worse in the next few weeks, it is unlikely to dislodge the Fed from the path it has now firmly chosen.

This I think is broadly consistent with views on the FOMC and explains why many policymakers insist that a rate hike this year remains likely. Vice Chair Stanley Fischer was the latest to reiterate the point. Via his prepared remarks for the IMF:

In the SEP, the Summary of Economic Projections prepared by FOMC participants in advance of the September meeting, most participants, myself included, anticipated that achieving these conditions would entail an initial increase in the federal funds rate later this year.

They will want look through any near term GDP volatility, and discount volatility related to inventories. Look then to real final sales rather than GDP. Avoid getting caught up in the headline numbers; watch the underlying trends instead.

Still, there is a range of views on the FOMC, from Richmond Fed Jeffrey Lacker, who believes the Fed should already have raised rates, to Minneapolis Federal Reserve President Narayana Kocherlakota, who would like the Fed to consider a negative rate. And arguably even the center is not particularly committed to a particular policy path. To be sure, they like to talk tough, but every time they get ready to jump, they walk back from the edge.

Why the lack of conviction? Essentially, the economy is resting on what is likely its high water mark for growth in this cycle, leaving the Fed perplexed regarding their next move. They want the economy to slow from its current pace and glide into a soft landing. But acting too early will leave their job half finished and sow the seeds of the next recession. Acting too late, however, will yield the inflationary outcome they so fear. And they don’t know the exact definitions of “too early” and “too late.”

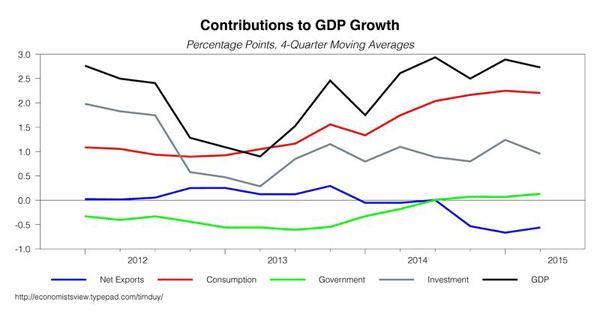

This chart (modified from Davies’ version) illustrates the evolution of US growth since 2012:

In broad terms, consumption, investment, and government spending jointly accelerated during 2013. The external side of the economy offset some of this acceleration by first moving from a slightly positive contribution to none and then, beginning in 2014, a substantial negative contribution. The net effect is that overall economy largely normalize around a 2.5% growth rate in 2014 and remained there since.

That 2.5% growth is what the economy delivers given the combination of long-term factors (labor and productivity growth) and the current set of fiscal, monetary, and external conditions. The actual composition of output will evolve around that 2.5% rate. It is likely the high-water mark, in terms of growth, for this recovery. Faster growth likely requires a net easier combination of monetary and fiscal policy. Slower growth may already be locked in by past policy, or maybe the economy just moves generally sideways from here.

Most important is to remember that monetary policymakers expect and want the economy to slow as it gently glides down to that mythical soft-landing. They aren’t looking for faster growth. The current pace of growth will, in their view, force unemployment further below the natural rate next year than they are willing to tolerate. Hence the most recent employment reports are not necessarily unmitigated bad news from their perspective. New York Federal Reserve President William Dudley, via Bloomberg:

Dudley said the key to liftoff will be whether the labor market continues to improve, thereby putting more upward pressure on wages and inflation. Last month’s jobs report was “definitely weaker,” but even monthly gains of 120,000 or 150,000 are enough to continue to push the U.S. unemployment rate lower, he said.

Or, more explicitly, from San Fransisco Federal Reserve President John Williams:

The pace of employment growth, as well as the decline in the unemployment rate, has slowed a bit recently…but that’s to be expected. When unemployment was at its 10 percent peak during the height of the Great Recession, and as it struggled to come down during the recovery, we needed rapid declines to get the economy back on track. Now that we’re getting closer, the pace must start slowing to more normal levels. Looking to the future, we’re going to need at most 100,000 new jobs each month. In the mindset of the recovery, that sounds like nothing; but in the context of a healthy economy, it’s what’s needed for stable growth. (emphasis added)

Williams is looking for 2% growth in the second half of this year and next year. He expects the economy to slow, and believes it needs to slow to sustain healthy, long-run growth. But I don’t think he knows exactly when and how much the Fed needs to tap the breaks to achieve that healthy growth. And he would not be alone – lack of consensus around the question is exactly why communication appears so muddled. They can’t tell you what they don’t know.

Further confusing the issue is the cat that Kocherlakota let out of the bag last week:

In mid-2013, the FOMC announced its intention to taper its ongoing asset purchase program. We can see that this announcement represented a dramatic change in policy from the sharp upward movements in long-term bond yields that it engendered. Personally, I interpret this policy change back in 2013 as the onset of what the Committee currently intends to be a long, gradual tightening cycle. As I noted earlier, we would typically expect that such a change in monetary policy should affect the economy with a lag of about 18 to 24 months. Viewed through this lens, the slow rate of labor market improvement in 2015 is not all that surprising.

I believe the FOMC should take actions to facilitate a resumption of the 2014 improvement in the labor market by adopting a more accommodative policy stance…

As group, monetary policymakers have stuck by the line that “tapering is not tightening.” Kocherlakota is not following the party line. He explicitly connects the dots and concludes that the current inflection point in the economy is the result of the tapering debate begun over two years ago. He essentially argues that had it not been for the taper and end of QE3, then financial conditions would be more accommodative today and the economy would not yet be at an inflection point.

Kocherlakota is an outlier; he is not interested seeing the labor market throttle back just yet, fearing that such an outcome will end improvement in underemployment indicators. This would lock the economy into a suboptimal state of persistent excess slack and impede the return of inflation to the Fed’s target. The general consensus on the FOMC is that such a goal can be achieved with more a more moderate pace of improvement in labor markets that holds unemployment modestly below the natural rate for a time. Hence he is alone in his view that more easing is needed at this time. Chicago Federal Reserve President Charles Evans probably comes closest with his explicit calls to hold rates at current levels until the middle of 2016.

But even if the party line is that “tapering is not tightening,” Kocherlakota must have planted the seeds of doubt in the minds of his colleagues. After all, it is a risk management exercise. If they are wrong, and Kocherlakota is right, then they will look like the dropped the ball if they pull the trigger too early. Something of a big risk to take when inflation remains persistently below trend and you lack traditional tools to respond to a renewed slowdown in activity.

Bottom Line: So where does all of this leave Fed policy? Confused, I think, like September when economists saw the outcome of that meeting as a coin toss. Don’t expect communications to become much clearer. October is off the table (despite what Lacker might believe). They first need to decide if the last two months of jobs data were aberrations or signals of slowing job growth. They can’t do that before October. And I am not confident they can do so by December. If we get two more reports hovering around 200k a month between now and December, matched with generally consistent data across other indicators, then December is on the table. That would indicate the economy is not coming off its high water mark without some help from the Fed. If jobs growth slows to 100k a month, again with a broad swath of generally consistent data, then we are looking at deep into 2016 before any hike. Around 150k is the gray area. They won’t know if the economy is poised to head lower on its own, or if that is sufficient to contain inflationary pressures. They don’t know if they should be tapping on the breaks or not. Risk management under the assumption of constrained inflation suggests they push off action until January or March. But they would not send such a clear message. Indeed, I suspect that more numbers like the last two will make the December meeting much like September’s. That I fear is my current baseline – another close call in which the Fed concludes to take a pass.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply