Well, the big day is finally here, and it’s not begun terribly auspiciously. Macro Man is desperately trying to fend off a headache, as the brackets supporting his six computer screens have completely packed in this morning. The rather cubist array of monitor angles is eerily reminiscent of a Picasso painting; while that’s fine for the Museu Picasso, Prado, or some other repository of the artist’s work, it’s not really what you want when you’re attempting to track the progress of hundreds of small, flashing numbers.

The larger question, of course, is whether this evening’s Fed announcement will generate headaches of an altogether more substantive sort. For choice, Macro Man suspects not; while there is some talk of the Fed starting to look at using reverse repos to drain liquidity from the system, this appears to be laying the groundwork for such a development next year rather than a sign of imminent draining. After all, there’d be little point in draining the SFB roll-off in the next couple of months when the MBS purchase program will be simultaneously increasing bank reserves.

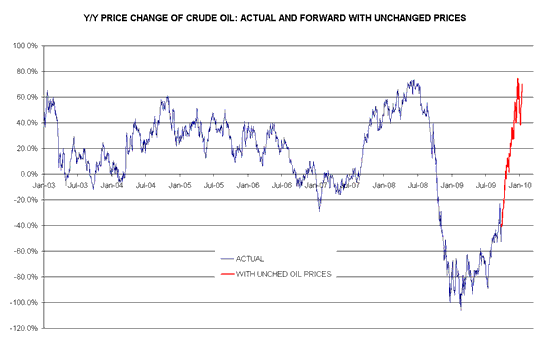

That having been said, the FOMC will be looking at a headache of its own before too long. The deflationary impact of commodity prices, particularly energy, is already waning; by the end of the year, unchanged oil prices will generate a similar magnitude of yearly gains that a) lured the ECB into its ill-fated July 2008 policy tightening, and b) immediately preceded last autumn’s global meltdown.

While it’s certainly not axiomatic that a similar outcome will ensue, particularly in the absence of further marginal oil price rises, the impact of base effects on reported CPI and PPI inflation should be fairly substantial. Those Fed voters who interact with actual businesses who pay actual energy bills may eventually prove to be a headache for the more academically-inclined Fed governors who tend to rely on output gap models and measures of “core” inflation.

And that could prove to be a headache for those managers reliant on short-vol or coupon-clipping strategies. To be fair, “risk on” and carry trades have been the nonpareil money-spinners of the past few months. Anecdotally, Macro Man’s sense is that just about every macro manager out there has some of the latter, even if they have disbelieved or attempted to fade the former.

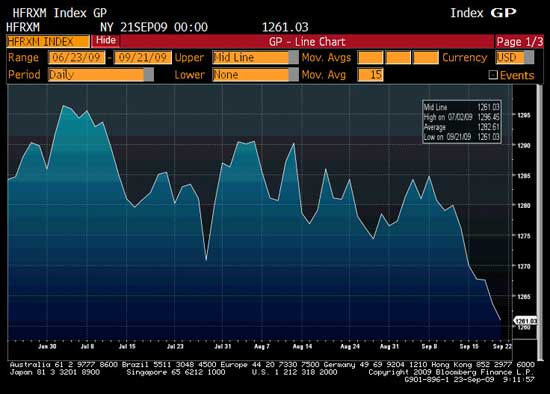

For what it’s worth, however, the HFR macro index has registered a pretty poor performance thus far this month. While Macro Man has certainly scuffled, there’s been enough juice in the carry trades, some of his long-risk equity trades, and the dollar to avoid a shocker. He’d have thought others were in a similar boat, but on the evidence of the chart below, perhaps not.

Macro Man has long thought that the last few months of the year would prove volatile and topsy-turvy as the risk rally comes under the threat of its own success (via the implied policy tightening that it would produce.) Thus far, it’s been fairly plain sailing. And while Macro Man is still positioned for the good times to continue, he’s started to rein in his horns a little so as to avoid the mother of all migraines if the Fed does change its tune.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply