As I have talked about or written on topics, I have learned that there are hot-button issues that almost always attract firestorms. Thus, when I write about Tesla, Apple or Facebook, I am guaranteed to provoke reactions, some strongly supportive and some strongly opposed, some rational and some emotional, but these reactions, for the most part, are determined by the pre-dispositions of the readers, rather than my views. In fact, my posting acts like a Rohrsbach test, with readers taking a portion of the post that is in line with or opposed to their positions, and either ignoring or discarding the rest of what I have to say. That, in part, is why I have stayed away from posting on Bitcoins, even as news stories about it, good and bad, have hit the headlines, since the world seems to be divided among the true believers in Bitcoins (who will brook no disagreement) and the cynics (who consider anything positive that is said about it to be a sign of gullibility). Since I live in a world filled with shades of grey, rather than black and white, I am going to try to look at the middle ground, though I undoubtedly will make neither side happy.

Bitcoin is a currency! And it cannot be valued!

Warren Buffet is already on record as saying that Bitcoin is “not a currency, because it does not meet the criteria of a currency, including being a store of value”. I guess I must have a lower standard than Mr. Buffett, because my criterion to classify something as a currency is that it be accepted in transactions. It is true that by my definition, shells and beads would have once been considered to be currencies and that is true. Perhaps, Buffett’s point is that Bitcoin is not a good currency or that it is one that will not stand the test of time, and those are certainly relevant and debatable questions,

Unlike an asset or a business which generates cash flows, a currency is a measurement unit that cannot be intrinsically valued. You cannot construct a DCF model to conclude that the US dollar is cheap or that the Chinese Yuan is expensive. However, it can be priced, at least relative to other currencies. With paper or fiat currencies, that pricing of course takes the form of exchange rates and the question about a paper currency’s pricing becomes one of determining whether the prevailing exchange rate is a fair one. However, not all currencies are paper and some non-paper currencies have been in use for centuries. The most obvious of these non-fiat currencies is gold and in a prior post, I argued that gold cannot be valued but that it can be priced, relative to paper currencies and that the pricing can be traced to fundamentals. Using the same logic, I will argue that while it is impossible to value Bitcoin, it is possible to view its price as an exchange rate into paper currencies and make judgments about whether the pricing is fair, again on a relative basis.

The determinants of a currency’s price

To make judgments on both the efficacy of Bitcoin as a currency, and indirectly, its staying power and pricing, I looked at three determinants of a currency’s price/power: the trust you have in its issuing entity, its acceptance in transactions and how securely you can store and save it, while generating a fair rate of return while doing so.

1. Trust in the issuing authority

The first factor that determines a currency’s price is the trust that users of the currency have in the issuing authority to keep its supply in check, with greater trust going with greater willingness to use and hold on to that currency. With paper currencies issued by governments, the authorities are usually the central banks in question: the Federal Reserve for the US dollar, the European Central Bank (ECB) for the Euro and so on. With gold or physical currencies, the constraint is usually a physical one, insofar as the supply of these physical currencies is limited by nature. Since anything that releases that physical constraint will render that physical asset useless as currency, it is ironic that alchemists have, for centuries, tried to make gold in laboratories, because their success would have undermined the use of gold as a currency.

So, what is the issuing authority for Bitcoin? There is none! While that may seem like a fatal weakness, the innovative aspect of Bitcoin is that while the power is spread across the network of users of the currency, the supply is set by a computer algorithm, which, in turn, cannot be changed by any user or even a group of users. If this sounds too complex, and it was for me, you may want to go back to the source, which is the paper that gave birth to the idea (by Satoshi Nakamoto). If the name sounds familiar, it is because it is back in the news again, with the controversial story in Newsweek last week, claiming to have unmasked the real Satoshi Nakamoto, with that person claiming in response that he was not the inventor of the Bitcoin. I must confess that the technicalities in the paper went over my head and I found this YouTube description of how it works to be a good one, though it is from the perspective of someone who is a Bitcoin believer.

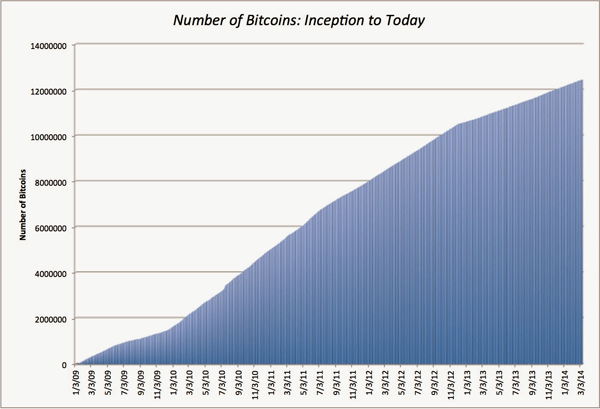

If you are still confused, let’s cut to the brass tacks. The supply of Bitcoins is constrained by the computer algorithm, which, as constructed, is (supposedly) very difficult to hack or change, because it requires collusion or agreement across the entire network. If the algorithm remains untouched, the increase in the number of bitcoins is therefore on autopilot (with about 25 created every ten minutes), as evidenced by looking at its history:

There were 12.4 million bitcoins in circulation in March 2014 and that number will rise, on the preset path, to reach a cap of 21 million bitcoins in 2140. The way in which people can acquire one of the new bitcoins is by mining for them, running powerful computers, as described in this article in the New York Times. As more and more people try to mine for these bitcoins, though, the difficulty of finding bitcoins has become greater over time.

The first key question with Bitcoin or any digital currency is whether people will trust a computer algorithm. While your first reaction may be “Hell, No!”, it may be worth asking yourself a different set of questions:

(a) Do you trust central bankers?

(b) If so, do you trust some central bankers more than others?

(c) Are these some computer algorithms that you would trust more than some central bankers?

My answers to these questions would be (a) not really, (b) of course and (c) yes. The rise of Bitcoin in the last four years has coincided with the Age of Hubris in central banking, where central bankers have donned Supermen capes and viewed their mission as saving economies, rather than protecting their currencies. It is also worth speculating whether money that would have normally flowed to gold, historically the prime beneficiary of loss of trust in central banks, has flowed instead into Bitcoin, explaining both the anemic price behavior of the former and the heady price action in the latter.

Bitcoin’s staying power will ultimately depend upon how impervious its source algorithm is to mischief. While Bitcoin’s defenders are quick to argue that its computer fortress is impossible to breach, this article seems to suggest that there are potential flaws that may be exploited by a collusive group. I am an absolute novice when it comes to computer technology of this type and I don’t know how much weight to attach to the claims in the article, but if you are a Bitcoin promoter, you want to make sure that even the slightest doubts that the algorithm can be fudged or modified are dealt with quickly and openly, since those doubts will undo its effectiveness as a currency.

2. Acceptance in Transactions

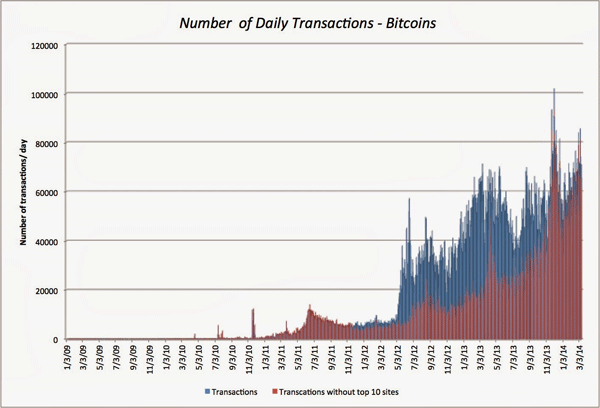

Since the defining role for a currency is that it can be used in transactions, the price of a currency will depend upon how widely it is accepted in transactions for goods and services. Promoters of digital currencies, in general, and Bitcoins, in particular, argue that they have two advantages over paper currencies: lower transactions costs and anonymity. However, the proof is in the pudding, and the chart below looks at the growth in the volume of Bitcoin transactions since inception:

Clearly, there are more Bitcoin transactions now, than ever before. Having never used Bitcoins in transactions, I was curious about how it worked and this link was pretty useful to get started, as I proceeded to build my bitcoin identity. I first created a digital wallet on my computer, which generated my first and subsequent bitcoin addresses. I then went to coinbase, one of many vendors of Bitcoins, to acquire my first Bitcoin, and after realizing that it would cost me $640, decided to check on where I would spend that Bitcoin by visiting this site that lists vendors that accept bitcoins in transactions. The good news is that transacting with Bitcoins is a breeze: you create an address for the transaction that you swap with a vendor who accepts it, and it is recorded in a transaction log called a block chain. The bad news is that vendor list is still limited, even in the US, and non-existent in many other parts of the world.

So, who are the primary users of Bitcoins? At the risk of over generalizing, the charitable view is that it is the young and technically savvy, the cynical view is that it is the paranoid and the secretive and the darkest view is that it is those who operate on the wrong side of the law. Fairly or unfairly, stories such as this one about Bitcoins being used in the drug trade feed into the perception, leading to legislative hearings and bans by some countries. (It is revealing that the countries that have cracked down on Bitcoins first are China and Russia. Perhaps, they feel more threatened by their inability to track what their citizens do and where they spend their money than other countries do.)

In summary, Bitcoin is a currency, but one that is currently accepted only in a small subset of transactions and used by only a few. Whether it or any other digital currency will be widely accepted will depend in large part on how its advocates package and market it. If the emphasis is on convenience, low cost and transaction speed, it has the potential for much wider acceptance, especially if it is made simpler to understand and not oversold. If the focus is on privacy, security and anonymity, I am afraid that the dark side will win out and it will become the currency of the paranoid and illegal, with all of the associated costs and benefits.

3. Security, Conversion, Storage and Rate of Return

The final measure of a currency’s strength and durability is how easily you can convert it into other currencies, how securely you can store and save it and and whether you are compensated while you hold it. The global currencies of trading, such as the US dollar or Euro, offer these benefits, since they can be converted at minimal cost into other currencies and can be invested in banks or securities to generate a market-determined rate of return, while idle. Emerging market currencies are more constrained, sometimes because they are restrictions on conversion into other currencies and often because they cannot be used or invested outside their local economies. Gold offers an interesting anomaly. While it can be converted into other currencies in most parts of the world, there are restrictions on trading gold in some countries, and holding gold does not offer any explicit returns other than potential price appreciation.

You can save your bitcoins on computers, but can you do so securely? It is possible that the stories about bitcoins being stolen from supposedly secure servers are overblown and that the recent collapse of Mt. Gox (one of Bitcoin’s biggest exchanges) was an aberration, but it seems to me that if these servers/exchanges are the equivalent of banks in the Bitcoin economy, these banks are unregulated and depositors have neither protection nor insurance against either bank runs or bank robberies. While it may conflict with the vision of some Bitcoin revolutionaries, the Bitcoin economy may need a banking system of its own that is regulated and perhaps even insured by a centralized entity.

A Comparison of Currencies

To get a measure of Bitcoin as a currency, I decided to do a comparison with three paper currencies (the US $, the Chinese Yuan and the Argentine Peso), a real currency (gold) and a digital currency (Bitcoin). Note that these are my subjective judgments and that you should free to substitute your own to come to your own conclusions.

(click to enlarge)

So, what do I get out of this table? Given my perceptions of how these currencies measure up on three three dimensions of currency quality, I would choose to be paid in US dollars over being paid in Chinese Yuan, and in Chinese Yan over Argentine Pesos. While I trust Nature more than any central bank when it comes to self-restraint, the lack of market-determined returns from holding gold would tilt me towards holding US dollars over holding Gold, but it is a closer call than it was five years ago. I would rather be paid in gold than in Yuan, though I would still be more comfortable with Yuan than Bitcoins. Finally, and I apologize in advance to my Argentine friends if they are insulted by this statement, but I am afraid that I would rather be paid in Bitcoins than Argentine Pesos today.

Bitcoin: To Buy or Not to Buy?

Now, for the $640 question! Would I buy Bitcoin at today’s price? No, and not because I am a Luddite that is convinced that digital currencies will not work. It is because I have never been good at calling currency movements and consequently have never bet on them. Since I would not bet on the dollar strengthening relative to the Euro or on the future price of gold, why would I try to do so with Bitcoin?

I believe that there will be a digital currency in wide use a decade or two from now. The question, of course, is whether that digital currency will be Bitcoin or a competitor. If you are a Bitcoin enthusiast, the pathway to its success requires three developments: the computer algorithm underlying the currency has to stay transparent, robust and protected, the usage of Bitcoins has to spread beyond the narrow band of enthusiasts to the broader marketplace and the infrastructure for securing, transporting and saving Bitcoins has to be strengthened. That will require true believers to accept compromises to both their vision (of a truly decentralized currency with no regulatory authorities or power) and their practices (anonymity, for instance, might become a casualty to commerce). Anarchy is a great disruptor of the status quo, but long-lasting currencies require order and predictability, and Bitcoin’s biggest promoters seem to have little fondness for either.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

WB has shown an aversion to Internet businesses, we can pull out statements all over where he says he simply doesn’t understand. To quote WB In that 2001 letter, Buffett said: “At Berkshire, we make no attempt to pick the few winners that will emerge from an ocean of unproven enterprises. We’re not smart enough to do that, and we know it.”

Given this admission and his aversion to all things Internet I think we can safely dismiss his comments as irrelevant as by his own admission he doesn’t really get it.