The late-summer holidays are finally over, and now it’s time to get stuck into a theme. The early returns (which admittedly cannot necessarily be trusted beyond, er, lunchtime today) suggest that theme is one of “reflation.”

On the face of it, today’s trading might suggest “dollar going down forever”, if not “dollar crisis.” Yesterday the UN, acknowledged experts in financial mismanagement and iniquity, issued a report trumpeting the need for a new global reserve currency, reviving an old chestnut guaranteed to set currency traders’ pulses racing.

Throw in the news of a long-overdue Hong Kong-listed sovereign debt issue from China, and the alternatives to the dollar look even more enticing. Sure enough, Macro Man’s currency screen is a sea of red (for the dollar), as it’s fallen against everything under the sun (other than the ILS, which has seen CB intervention.)

So is it another incipient dollar crisis, then? Not so fast, my friend! If there were a dollar crisis brewing, shouldn’t Treasuries be selling off rather than remaining bid? In fact, the price of everything seems to be going up, at least measured in dollar terms.

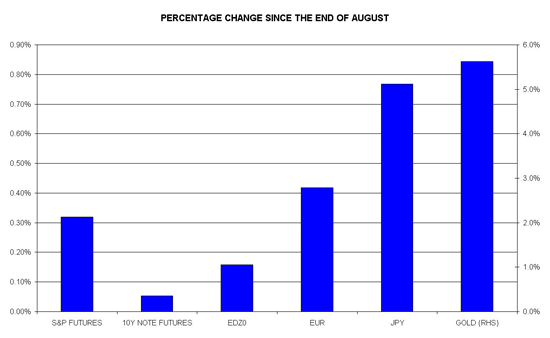

The chart below plots the return on six different asset prices- S&P futures, 10y Treasury futures, EDZ0, gold, the EUR and the JPY- since the end of August. As you can see, they’re all higher.

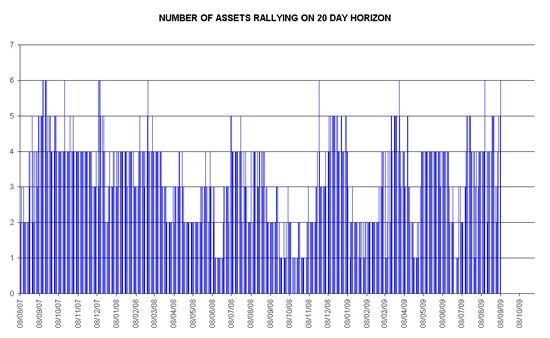

This trend has actually been persisiting for a bit longer than the last week…Macro Man plotted the rolling 20 change of these six prices since the start of the financial crisis, and totted up how many of the six were positive. Sure enough, as of this morning all six of ’em were up over 20 days ago.

Over the past two plus years, this has actually been a fairly rare phenomenon: we’ve registered a +6 on just 14 of 545 days, or 2.6%. And most of those were in the aftermath of the initial Fed rate cut in September, which as you may recall exceeded expectations at the time. Indeed, since the end of 2007 three have been less than half-a-dozen times when the all six of these asset prices have risen together on a 20 day horizon.

What should we take from this? That the theme du jour is likely to be exactly that, soon to be replaced by something else that will encourage asset market returns to go their separate ways? That monetary velocity has yet to show any signs of picking up would argue in favour of this proposition.

Then again, if economic actors are going to start using the huge pile of dollars (and other currencies) that central bankers have dropped from their respective helicopters, mightn’t it show up in asset pricing before it hits the official economic data, even on money supply?

So this is the conundrum that Macro Man is wrestling with this morning. His eyes tell him that it’s just a big reflation trade. Yet consensus, his own expectations, and the weight of the last 21 months’ experience warn that recent price action is just a head fake. But the W-shaped macro consensus is so firmly entrenched that it might need a few weeks of contrary price action to shake things up before re-asserting itself when it’s not expected.

Decisions, decisions, decisions. Macro Man is trying his best to hedge his bets, keeping his core view intact within his portfolio while still trying to participate in the speculative orgy of “everything goes up.” It’s easier said than done, especially when there’s a change in cross-asset correlations and volatility.

It’s all a bit tricky when you don’t know if you’re trading the theme du jour…or the theme d’annee….

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply