As we all become more familiar with the IB Probability Lab, certain market anomalies can become evident. There appears to be one in the January 2015 options in Tesla Motors (TSLA).

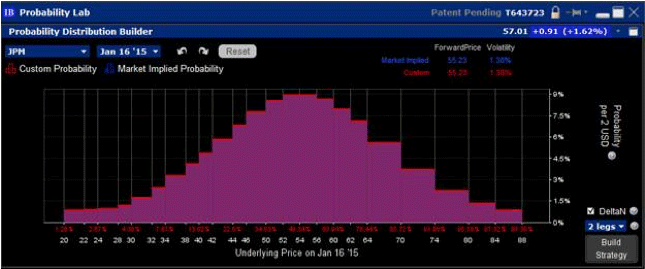

Within the context of the options market, anything over a year is considered long-term. While that may epitomize short-term thinking, a year can seem like an eternity when holding a decaying asset. The options market tends to take a fairly benign view of the long-term prospects of most blue chip companies, as evidenced by the probability curve for JP Morgan (JPM):

(click to enlarge)

The probability distribution is clearly centered on a forward value that is consistent with a low risk-free interest rate and roughly $2 in anticipated dividends. This pattern is typical for the January 2015 options across a broad range of widely held stocks.

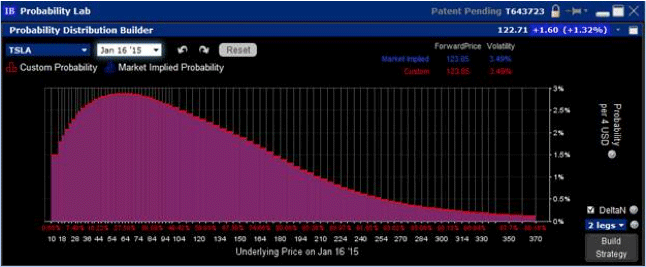

Compare the JPM chart above with that of TSLA, below:

(click to enlarge)

It is instantly apparent that the market imputes a much higher likelihood of negative outcomes for Tesla’s stock price. More than half the outcomes are below the current stock price (using the cumulative percentages displayed in red just below the X-axis), and the market implies the single most likely outcome to be a price of about $64, a nearly 50% drop from here. While the market attributes roughly a 9% likelihood of JPM having a generally unchanged stock price (allowing for dividends), TSLA options imply only about a 2% chance. That isn’t too surprising, since TSLA is much more volatile than JPM, but it is unusual to find a stock where there are severely negative outcomes that are far more likely than remaining roughly unchanged.

The implied forward price tells a somewhat different story, however. It may appear that the options market is implying a much lower forward price for TSLA, based on the concentration of probabilities around a much lower stock price. Yet the market implied forward price is over $1 higher! Despite a smaller cumulative probability of a higher stock price, the small but finite probabilities across the enormous range of upside strikes combine to push the forward price above the current market price.

There is a confluence of factors that are somewhat unique to TSLA that account for this unusual display. On the upside, there are not many stocks that have strikes so far above the stock price. When TSLA was trading above $190, up from $40, a $350 strike may not have seemed so outlandish. On the downside, the market appears to have a long memory of the stock-loan difficulties that surrounded TSLA earlier this year. During the spring, the stock loan rate for TSLA approached -50% (if you could actually locate shares to borrow). When the stock began to trade consistently around $100 in June, the availability of borrows improved and the stock-loan rates began to approach 0%. Although the stock-loan rate has generally been in the -3% to 0% range since then, and borrows are consistently available, it seems as though many options market participants remain fearful that borrowing difficulties could resume at some point in the next 13 months. That could explain their willingness to aggressively price their downside protection, implying high probabilities of a stock price decline.

How you choose to trade this anomalous market is up to you. Rather than suggesting how I see the potential outcomes, I encourage traders to first decide whether they agree with the probability distribution implied by the market. If you disagree, adjust the bars in the Probability Lab to levels that seem more sensible, and let the Strategy Selector help you to decide. One piece of advice – if you simply lower the upside, it will actually imply an even higher likelihood of a downside move, and vice versa. If you are more market neutral than current prices imply, you would need to raise near money strike probabilities as well. It isn’t always obvious that for a user to imply a lower overall volatility, he would need to raise the likelihood of near money outcomes.

Leave a Reply