The FOMC meeting concluded largely as anticipated, with a tempered downgrade of the economic assessment from “moderate” to “modest” and a new warning about the dangers of low inflation. Of course, given the weak first half evidence in the GDP report, “modest” seems like an appropriate adjective. In addition, the Fed highlighted the recent rise in mortgage rates, signalling their concern about negative feedback effects. Treasuries gained the news, wiping out earlier losses.

That said, there was no sense that the general forecast had changed dramatically. The Fed still expects activity to pick up in the second half of this year, and likely still expects that that pickup will be sufficient to require the withdrawal of accommodation, beginning in the next few meetings, with September still the consensus. They will be looking for data that supports that expectation. It is mostly likely the case that strong data for July and forward will be more important than weak data from June and back.

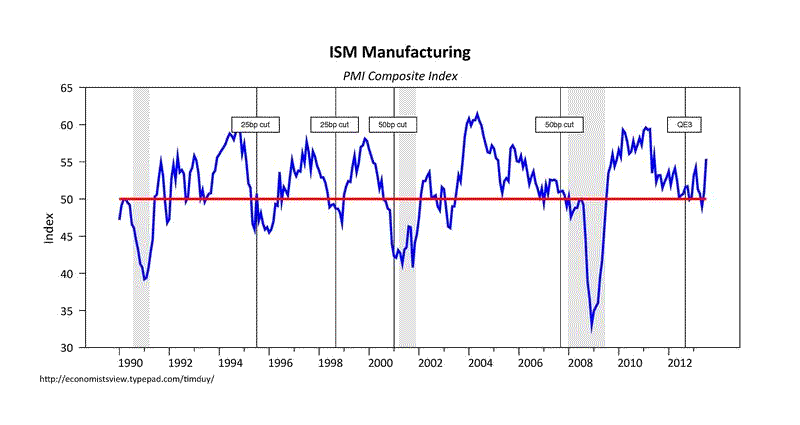

With that in mind, the early data is looking good for tapering sooner than later. Treasuries reversed yesterday’s gains this morning on the combined strength of the ISM manufacturing and initial claims reports. Manufacturing received a boost in July:

(click to enlarge)

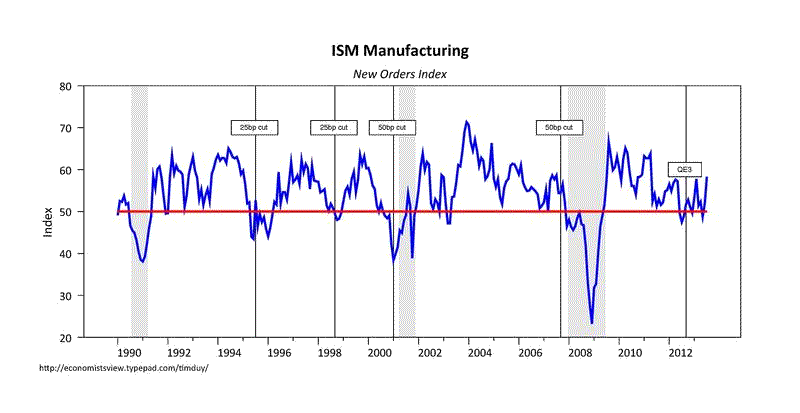

Moreover, the underlying components were solid as well. New orders rebounded:

(click to enlarge)

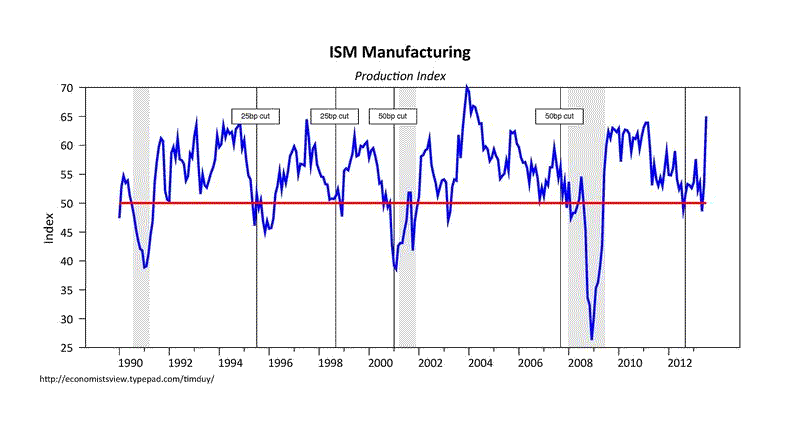

Production surged:

(click to enlarge)

And employment gained:

(click to enlarge)

It looks like something lit a fire under the manufacturing sector last month. In addition, initial claims surprised positively:

(click to enlarge)

I would say the general downward trend of the last year remains intact. More positive employment news came yesterday with the ADP report showing a private sector job gain of 200k for July. While Calculated Risk is correct that the ADP report is not particularly useful in predicting the initial release of the nonfarm payrolls numbers (which could be all over the place), Joe Weisenthal is correct in that it does track the underlying trend of the labor market, and signals that recent strength continued to hold. Moreover, regarding tapering, employment is probably still the most important data.

Bottom Line: Early signs look good that the first half doldrums are easing. But early signs are just that, early. For example, tomorrow we get the employment report, which can be notorious volatile. Moreover, we still have a wealth of data between now and the next FOMC meeting. But if early data is any indication where the economy is heading, the FOMC will shift further toward reducing monetary accomodation between now and the next meeting.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply